Asset Location

Asset Location for Tax Minimization

The strategic approach of asset location plays a crucial role in optimizing investment portfolios by minimizing tax liabilities and ultimately enhancing after-tax returns. While asset allocation, which involves distributing investments across various asset classes like stocks, bonds, and cash based on risk tolerance and financial goals, is a fundamental pillar of portfolio management, asset location takes this a step further by considering where these assets are held. By carefully matching investment types with the most tax-efficient accounts, investors can significantly improve their overall financial outcomes.

Understanding Account Types and Asset Tax Efficiency

To effectively implement an asset location strategy, it's essential to understand the tax implications of different investment accounts and asset classes:

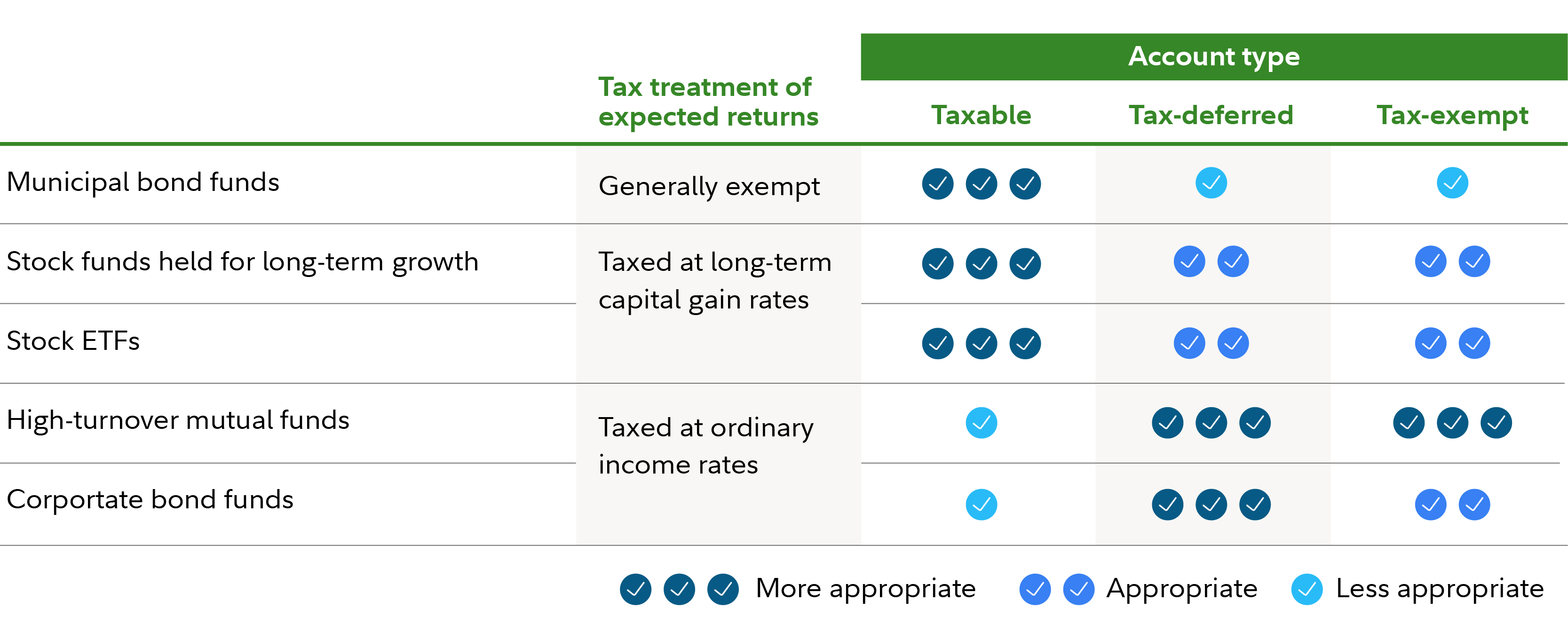

- Account Types:

- Taxable Accounts: These include standard brokerage accounts. Investments held here are subject to taxes annually on interest, dividends, and capital gains (when assets are sold for a profit, or tax inefficient mutual funds that distribute a gain without you selling).

- Tax-Deferred Accounts: Examples include traditional 401(k)s and Individual Retirement Accounts (IRAs). Contributions to these accounts may be tax-deductible, and investments grow tax-free until retirement, at which point withdrawals are taxed as ordinary income.

- Potentially Tax-Exempt Accounts: Health Savings Accounts (HSAs), Roth IRAs, and Roth 401(k)s fall into this category. Contributions to Roth accounts are made with after-tax dollars, but qualified withdrawals in retirement are entirely tax-free. HSAs offer a triple tax advantage: tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses.

- Asset Tax Efficiency:

- More Tax-Efficient Assets: These are investments that typically generate less taxable income or benefit from preferential tax treatment. Examples include municipal bonds, whose interest income is often exempt from federal and sometimes state and local taxes, and stocks held for over a year, which qualify for lower long-term capital gains tax rates.

- Less Tax-Efficient Assets: These assets tend to generate higher amounts of taxable income or have less favorable tax treatment. This category often includes high-turnover stock mutual funds, which can generate frequent short-term capital gains, and assets that produce interest income, such as corporate bonds or certificates of deposit (CDs), which are taxed at ordinary income rates.

Implementing an Asset Location Strategy

The core principle of an effective asset location strategy is to place less tax-efficient assets into tax-advantaged accounts (tax-deferred or potentially tax-exempt) and more tax-efficient assets into taxable accounts. This approach shields the income and gains from the most heavily taxed investments from current taxation, allowing them to grow more rapidly over time.

For example, a common strategy involves holding income-generating assets like bonds, Real Estate Investment Trusts (REITs), or actively managed funds that generate frequent short-term capital gains within tax-deferred accounts like a traditional IRA or 401(k). This protects the annual interest income or short-term gains from immediate taxation. Conversely, highly tax-efficient assets like Direct Indexes, ETF's, or low turnover mutual funds that can potentially qualify for long-term capital gains treatment, can be placed in taxable brokerage accounts. The lower tax rates on long-term capital gains and qualified dividends make these suitable for taxable accounts.

Complexities and Professional Guidance

While the concept of asset location is straightforward, its practical application can be quite complex, especially for individuals with diverse investment portfolios and multiple household accounts. Factors such as changing market conditions, evolving tax laws, and life events can all impact the optimal asset location strategy. Maintaining and rebalancing this strategy over time requires continuous monitoring and adjustments.

Given these complexities, collaborating with a financial professional is highly recommended. A financial advisor can conduct a holistic review of an individual's or couple's entire portfolio, assess their unique financial situation, and help craft a personalized asset allocation and location strategy. This professional guidance can ensure that investments are optimally positioned to achieve long-term financial goals efficiently and with minimal tax impact.